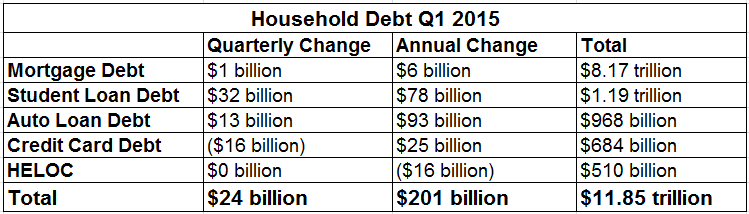

The Federal Reserve Bank of New York announced in its Q1 2015 Household Debt and Credit Report, that total household debt reached $11.85 trillion, up only $24 billion from last quarter. Growth in balances slowed across most categories for the quarter, most notably in mortgage balances, which grew $1 billion, down $38 billion from the previous quarter.

“Tight standards on mortgage lending are reflected in both sluggish growth in housing debt as well as substandard reductions in mortgage delinquency and defaults,” said New York Fed SVP and economist Andrew Haughwout.

“Tight standards on mortgage lending are reflected in both sluggish growth in housing debt as well as substandard reductions in mortgage delinquency and defaults,” said New York Fed SVP and economist Andrew Haughwout.

Credit card balances declined $16 billion after gaining $20 billion in Q4. Although the aggregate credit card limit increased by nearly one percent, new extensions of credit were slow as the number of credit inquiries dropped by 5 million from the previous quarter.

Delinquencies improved somewhat, as 5.7 percent of outstanding debt was in some sort of delinquency, compared to 6.0% in Q4. Mortgage delinquencies were 3 percent, 10 basis points lower than in Q4. About 112,000 individuals had foreclosure notation added to their credit reports, the lowest since the data was first collected in 1999.

Student loan debt drove the increase in total household debt adding $32 billion, a slight increase from last month. Although the 90+ day delinquency rate dropped 2 basis points, it remained high at 11.1 percent (and may actually be much higher since about half of these loans are in deferment). Given that there are $1.19 trillion in student loans outstanding, the economic consequences could be extraordinary

As Donghoon Lee, a research officer at the New York Fed noted in February, “Student loan delinquencies and repayment problems appear to be reducing borrowers’ ability to form their own households.” Approximately 8 million Americans are in default on their student loans according to the CFPB, with an additional 3 million Direct Loan borrowers at least 30 days past due. As the average amount of student loan debt and defaults continue to grow, an increasing share of borrowers may find it increasingly difficult to make large purchases.